Proof of Resiliency

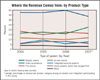

Security dealers and systems integrators describe how their 2007 total annual revenue is distributed among types of services. Non-residential sales and installation accounted for a greater share — up 5 percentage points — of total revenue in 2007.

Security dealers and systems integrators describe how their 2007 total annual revenue is distributed among types of products. The largest revenue-producing product category for SDM’s subscribers historically has been intrusion alarms, which comprised one-third of dealers’ total revenue, on average. The biggest upset, however, is the video surveillance category which gained 7 percentage points and accounts for an average 23 percent of dealers’ and integrators’ total revenue.

But considering the increasing sense of vulnerability that Americans feel about their safety and security, it should have been expected.

“I think we’re in a great period right now,” says Tim Whall, chief operation officer of HSM Electronic Protection Services, owned by The Stanley Works. The publicity surrounding security technology has made our industry a mainstream topic, he says.

“We’ve never been as close to the front page as we are now. We’re seeing that every year in our sales figures. There’s more and more opportunity out there,” Whall emphasizes.

These are the non-residential vertical markets in which SDM’s subscribers expect to have the highest rate of growth for their companies. The middle-market — especially commercial office space and retail — is the target dealers and integrators are aiming for in 2008.

For example, although the lowered level of residential construction has impacted security dealers that depended on prewired alarm system sales, many of these dealers have picked up business from customers that want to enhance their existing security systems with video monitoring and remote monitoring using cells phones and PCs. In the non-residential arena, boosting growth are technologies such as IP-based video, global positioning systems (GPS), and incident tracking and management.

The health and viability of the electronic security industry is measured each year through SDM’s Industry Forecast Study, conducted annually since 1981. The results of the study are presented in the tables and charts on these pages. Through the Forecast Study, which samples SDM’s subscriber base of installing security dealers and systems integrators, we get a depiction of the strength of the industry as measured by revenue increases and decreases, expected growth for the coming year, pricing trends for systems and services such as monitoring, and challenges that installing companies face such as employment issues and channel conflict.

SDM’s Forecast Study shows that dealers reeled in their reliance on new construction — a segment that fell by 12 percentage points — and instead will focus on existing middle-value and high-value homes.

STATE OF THE MARKET: EXCEPTIONAL

Overall, the state of the security market is exceptional, deem the respondents to SDM’s 2008 Forecast Study. When asked to consider the economic health of their businesses and the potential for sales in 2008 among various product categories, dealers and integrators indicated that video surveillance leads the way. More than 9 out of 10 (92 percent – up from 89 percent in last year’s Forecast Study) described the potential for video system sales as “good,” “very good” or “excellent.”

Considering the economic health of their businesses, security dealers and systems integrators ranked four of the industry’s primary product categories by their potential for sales in 2008. Ranked by mean averages, survey respondents chose video surveillance as having the highest potential for 2008 sales (rated a 3.90 mean average), followed by burglar alarm systems (3.46 mean average), fire alarm systems (3.26 mean average), and access control (3.24 mean average).

Alarm systems are the foundation of the security industry and historically have been responsible for the lion’s share of total annual revenue. However, SDM’s Forecast Study shows that each year since 1992, burglar alarms as a percentage of total revenue has dropped — while revenue from video surveillance systems has picked up in its place. An average of 33 percent of security companies’ total revenue in 2007 came from alarm systems (down from 40 percent in 2006), and 23 percent came from video surveillance systems (up from 16 percent in 2006).

“Economic conditions” remains very high on the list of factors that SDM’s subscribers feel will have the greatest impact on sales in 2008.

DOUBLE-DIGIT GROWTH

If your business grew last year, then you keep good company. And, if your total gross revenues grew by double digits, then you’re in line with industry norms.More than half (55 percent) of the security dealers and systems integrators who participated in the 2008 Forecast Study report an increase in 2007 revenues over 2006, and another 36 percent report even revenues with 2006. Only 9 percent declined.

Among respondents that improved, the average increase was 19 percent more. (Compare with 2006’s average 16 percent increase.)

To know exactly what is measured, survey respondents were asked to state their company’s revenue from the sale, lease, installation, service, and monitoring of security systems including alarms, access control, video surveillance, life-safety, home systems, and related low-voltage systems.

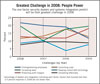

Finding and retaining employees will be the greatest challenge faced by security dealers and systems integrators in 2008, having grown in importance each year since 2005.

Respondents anticipate their top three best-growth markets in 2008 will be retail, commercial office space, and educational facilities on the non-residential side. On the residential side, they foresee growth coming primarily from existing homes in the middle-value range.

The top three equipment categories in which security dealers and systems integrators expect to increase their level of spending most dramatically this year compared with last year, are video surveillance/CCTV, monitoring equipment, and IP network-based video equipment.

TROUBLE BREWING IN THE CHANNEL?

Challenges are expected, with perhaps the most important ones being finding and retaining good employees and being aware of potential conflicts within the channel of distribution.

SDM’s Forecast Study collected RMR information for the first time in the survey’s history. The results show that there is a wide range of company sizes participating in the market, and provide a basis of comparison for future surveys.

Consolidation among manufacturers, as well as convergence of physical security technology and information technology providers, may be creating some channel conflict.

More about the Survey

The objective of SDM’s Forecast Study is to measure prior-year sales activity, revenues, business challenges, market opportunities, and other factors. In October 2007, SDM mailed a four-page questionnaire to a random sample of 2,000 SDM subscribers based in the United States, with a $1 incentive to complete the survey. In addition, a sample of 9,968 (non-duplicated) subscribers were e-mailed an invitation to complete the survey online, with an incentive of a drawing for a $250 gift check randomly selected from among all respondents. Respondents — who have executive management titles — returned their completed questionnaires to SDM in November 2007, and results were tabulated on a 4 percent response rate of usable returns.Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!