SDM EXCLUSIVE

Top Systems Integrators Report 2024: Transformative Change

July 3, 2024

SDM EXCLUSIVE

Top Systems Integrators Report 2024: Transformative Change

July 3, 2024

With supply chain shortages fading in the distance for many and an economy that held its own — in spite of predictions to the contrary — the 2024 SDM Top Systems Integrators were in an ideal position to benefit from the tailwinds of technology changes that had been starting to blow in pre-pandemic times but turned to a steady breeze after Generative AI hit the public consciousness in November 2022. With cloud, Security-as-a-Service, video monitoring, analytics and AI now top-of-mind for many customers, and more consistently available from manufacturers, these top 100 companies were able to meet their customers’ challenges and pain points head on — and the numbers tell that tale.

2024 SDM Top Systems Integrators Rankings Preview

This year’s group, collectively, took in an impressive $7.17 billion in North American systems integration revenue, the highest number since 2013 and a 9 percentage point increase over last year’s $6.54 billion. The number of companies reporting increased profit margins in 2023 also rose by 12 percentage points to 60 percent, with the average increase at 11 percent.

“Overall, 2023 was an amazing year,” wrote No. 64, Security Alarm Corporation. "Both 2022 and 2023 were very strong years. [But] 2023 was substantially better compared to 2022 in the installation and integration part of the business. There is still a decent amount of money circulating through government facilities, which contributed to the boost.”

This was a theme across many comments.

Top Systems Integrators: At a Glance

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

Top Systems Integrators: 10-Year Performance

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

Profit Margin Up

Top Systems Integrators were asked, “Did your company’s net profit margin increase, decrease or stay about the same in 2023 compared with 2022?”

// SOURCE: SDM OP SYSTEMS INTEGRATORS REPORT, JULY 2024

2024 Revenue Confidence Remains High

Top Systems Integrators were asked, “How do you expect revenues in 2024 to compare with revenues in 2023?”

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

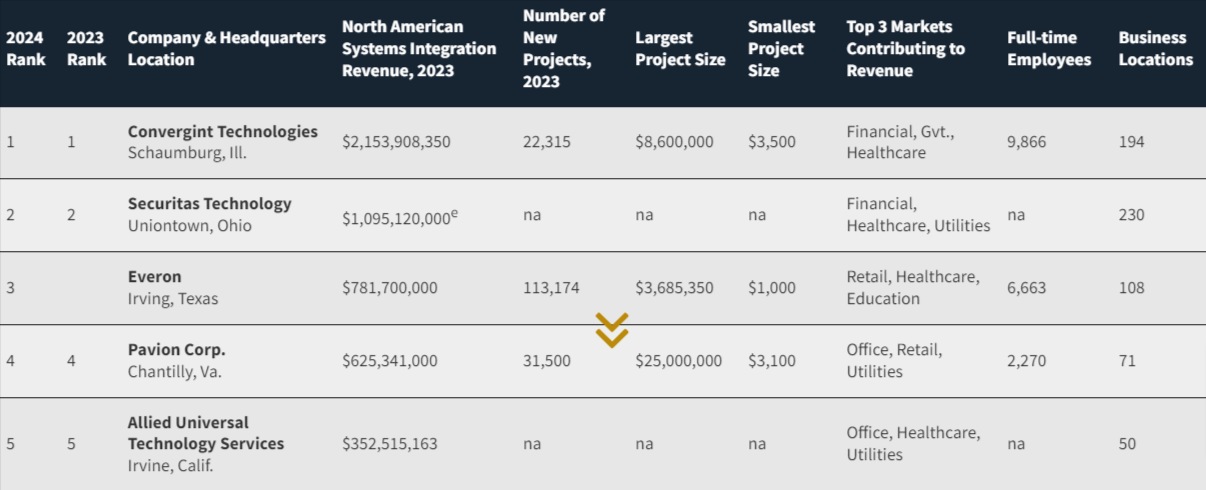

Top 10 Integrators by Total Revenue

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

Security Integrators’ Sales Revenue by Product Category

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

Security Integrators’ Sales Revenue by Service Category

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

Breakdown of Jobs on an Integrator’s Staff

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

94% of Fleet are Technical Vehicles

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

Top 3 Sectors Are Education, Office Space, Healthcare

// SOURCE: SDM TOP SYSTEMS INTEGRATORS REPORT, JULY 2024

No. 9, Pye-Barker Fire & Safety, wrote: “2023 was a stronger market for integrated systems projects than 2022. Supply chain has started to return to normal. Inflation was still there but not anywhere near as bad as it was in 2022.”

No 94, Pace Protection, wrote: “The market was very strong in 2023. The best growth we saw was in private schools, chains and banking institutions. Our company was not impacted by supply chain disruption or inflation in 2023.”

Many companies cited certain stronger verticals, but another common theme was the overall increased demand for new technologies and solutions.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

“Convergint achieved monumental growth in 2023, significantly advancing its service capabilities across audio-visual, fire and life safety, and healthcare integration resulting in a staggering $2.5 billion in global revenue,” wrote the No. 1-ranked company. “In 2023, the market for security systems was strong — driven by the escalating need for highly automated and AI-driven systems that can protect facilities and device networks from emerging threats (both physical and cyber).”

Technology demand accounted for a lot of the increased business, and many security integrators cited video monitoring, analytics and AI as some of the top requested solutions, as was also the case with this year’s SDM 100 Companies. Cloud-based hosted and managed solutions were also popular in 2023. While there are a few points of concern — notably inflation and an election year — the general consensus going forward is that these technologies will continue to rise in demand, as more end users face rising crime, active shooters, vagrancy issues and business needs that can be helped by these solutions.

As No. 25, Prosegur Security Integration, wrote: “Throughout 2023, the demand for security systems remained resilient, driven primarily by ongoing concerns regarding safety and security across various sectors. One notable trend in 2023 was the continued expansion of integrated security solutions. Businesses and organizations increasingly sought comprehensive security systems that seamlessly integrate various components such as access control, video surveillance, intrusion detection, and fire detection. This trend was particularly evident in sectors prioritizing robust security measures, including critical infrastructure, financial institutions, and large-scale commercial enterprises. The security industry is on the cusp of a dynamic transformation, with technology, integration, and adaptability at its core. We are committed to staying at the forefront of these developments, leveraging innovation to provide our clients with the highest level of security services and support.”

Market Drivers & Challenges

Much of what drove last year’s success was the awareness, demand, willingness and ability to pay for new technologies to solve emergent or ongoing security and business issues.

“In its Commercial and National Account Business Units, Guardian experienced growth in most verticals in 2023,” wrote Kevin Santelli, vice president of commercial and national accounts for the No. 39-ranked company. “These employers continue seeking new ways to efficiently manage multi-site locations and overcome labor shortages as evidenced by their ongoing investments into AI and cloud-based systems.”

No. 4, Pavion Corp., wrote similarly: “We are still seeing strong demand for technology refresh and upgrades as well as extension of services to improve business operations, enhance revenue and protect profits by strategically applying technology and emerging needs for AI offerings.”

This year’s top 100 systems integrators provided a lot of input on technology trends — particularly AI — and the impact they will have on the future of their business. Here is more on what they had to say:

- NO. 11, UNLIMITED TECHNOLOGY INC.: Artificial Intelligence (AI) remains a pivotal area of focus, critical for enhancing operational processes, minimizing errors, and fostering scalability. The evolving complexity of AI demands a higher level of expertise from integrators, who must keep pace with technological advancements to deploy and manage these systems effectively.

- NO. 15, STONE SECURITY: With the upward trend of crime and violent crime globally, elections may also have an impact on AI and cloud or SaaS solutions. Our industry is changing, it always has been, but with the advent of AI, it is changing seemingly faster today.

-

NO. 25, PROSEGUR SECURITY INTEGRATION: We anticipate several key trends and shifts in the security landscape:

- INTEGRATION OF TECHNOLOGY AND SECURITY: We expect to see continued integration of cutting-edge technologies such as artificial intelligence (AI), machine learning, and the Internet of Things (IoT) into security systems. These technologies will enhance real-time threat detection, monitoring, and response capabilities.

- CYBERSECURITY CONVERGENCE: The boundaries between physical and cybersecurity will blur further. Integrated security solutions that protect both physical assets and digital data will become increasingly critical in safeguarding organizations from comprehensive security threats.

- CLOUD-BASED SOLUTIONS: Cloud-based security solutions will gain prominence due to their scalability, flexibility, and accessibility. Cloud technology will enable real-time data sharing and analysis across multiple locations, enhancing security responsiveness.

- PREDICTIVE ANALYTICS AND AI-DRIVEN INSIGHTS: Predictive analytics and AI-driven insights will empower security professionals to proactively identify potential threats and vulnerabilities. This shift from reactive to proactive security measures will be pivotal in risk mitigation.

- REMOTE MONITORING AND CONTROL: Remote security monitoring and control will become more prevalent, allowing organizations to manage security operations from anywhere. This trend aligns with the increasing need for flexibility in response to global events.

- PRIVACY AND COMPLIANCE: As data privacy regulations continue to evolve globally, security providers will need to place a stronger emphasis on compliance and data protection to ensure the trust and confidence of clients.

- SUSTAINABILITY AND ENVIRONMENTAL CONSIDERATIONS: The security industry will increasingly prioritize sustainable and environmentally friendly practices. Energy-efficient security systems and eco-friendly technologies will become standard.

- CUSTOMIZED SECURITY SOLUTIONS: We believe clients seek customized security programs. The need for tailored security solutions will grow. Security providers will need to offer customizable services that address the unique needs and risks of each client.

- THREAT LANDSCAPE EVOLUTION: Threat actors will continue to adapt and evolve. Security providers will need to stay ahead by constantly innovating and enhancing their capabilities to counter emerging threats effectively.

- NO. 52, D/A CENTRAL: We are finally seeing more seamless integration of systems. The manufacturers are behind on integrating AI into their user interfaces, which will be critical for ease of use and reporting queries.

- NO. 87, OWEN SECURITY SOLUTIONS INC.: We believe AI will play a huge role in our business. AI will help make things more efficient and allow for more self-service options for the consumer.

No. 15, Stone Security, wrote that the integration business in 2023 was, “Very strong, with massive growth in standardization of modern yet tried, true and tested solutions. The theatrics of cloud security systems and analytics have caused peak interest of existing and new clients, and this has allowed Stone to consult and assist our current clients in the preparation of the future, for example deploying new and updated deep learning camera systems and exploring a hybrid of cloud + on-prem systems that truly integrate and interact with each other but are supported by our talented team.”

No. 30, Dallas Security Systems Inc. & DSS Fire, noted a greater focus on projects consisting of monthly subscriptions, including video monitoring, as did a number of others, including A+ Technology & Security Solutions, ranked No. 35, who noted an increase in demand for cloud/hosted solutions in 2023 as compared to 2022.

But not all was full steam ahead. The supply chain issues were waning throughout the year but still had an impact in some sectors. And inflation and high interest rates, despite not being an issue for some, were definitely a drag on business for others

No. 11, Unlimited Technology Inc., wrote: “In 2023, the market for security systems sales and integrated systems projects presented a varied landscape compared to 2022. The demand and interest in advanced technologies such as AI-enabled analytics, machine learning, SaaS solutions, weapons detection, and vehicle screening systems [increased], yet the industry faced significant challenges due to supply chain shortages, especially the global chip shortage. The utility market remained robust, driven by concerns over vandalism, vagrancy, and copper theft, which led to increased funding and project execution. However, the video surveillance market experienced delays in product availability, further exacerbated by chip shortages, resulting in extended lead times and affecting service levels across the industry. Despite these obstacles, areas leveraging AI and cloud-based solutions, enriched with advanced technologies like weapons detection and AI-driven analytics, experienced growth in 2023. The sector also observed increased interest in vehicle screening technologies, indicative of its rapid adaptation to the evolving landscape of security threats. Nevertheless, inflationary pressures led to tighter margins and price increases, impacting companies throughout the industry.”

No. 16, GSI, also wrote of inflationary disruptions: “Demand was stronger and equipment/material was more available than in 2022. Inflation was disruptive to our pricing model and we had to shorten the length of time for which our quotes were valid.”

And No. 31, Advanced Electronic Solutions, noted how inflation in the form of wage increases and equipment price increases led to “an increasingly complex operating environment.”

The talent shortage, another challenge mentioned frequently this year, is one that has been a thorn in the industry for the past several years and shows no sign of abating.

“No. 16., Zeus Fire and Security LLC, wrote: “We saw fewer supply chain disruptions in 2023 versus the prior year, but continue to face a shortage of skilled technician labor in most markets. … Our biggest challenge to grow will continue to be finding, attracting, and developing skilled labor to install and service our systems. We’re pursuing all available avenues to recruit and partnering with organizations that promote careers in the trades to help build the pipeline for the future.”

What’s Coming Next?

Looking ahead to the second half of 2024 and a bit beyond, these top 100 security integrators are still very optimistic, with a few caveats. Asked about expectations for their 2024 revenues compared to 2023, close to 80 percent expected them to increase, essentially the same level of optimism as last year.

But this year is also an election year, and with two major international wars in Israel and Ukraine, ongoing inflation and high interest rates, and continued rumblings about a recession, there are some causes for hesitation.

“Political and economic uncertainties have the potential to greatly impact our business,” wrote No. 21, American Alarm & Communications. “Weaknesses in our state’s economy as well as what happens with the wars in Ukraine and Israel, the presidential election, interest rates, the stock market, immigration policies — all these issues will affect funding/spending for the public and private sectors.”

No. 49, IP Systems Inc., wrote: “The state of the global economy will continue to be a crucial factor. Economic downturns or recessions can affect businesses’ spending capacities. The state of two wars with potentially widening geo-political impact is cause for concern.”

And No. 62, Visionary Systems, wrote: “The economy certainly has some people holding onto their money rather than spending it on large security projects. Although in a positive light, the general public continues to move towards the view that security is a necessity rather than a commodity.”

That last point is largely fueling the optimism of the majority of respondents, along with the boost in interest in cutting-edge technologies.

“In 2024, the following will have the greatest impact on our business: active shooters; crime/terrorism, legislation, grant and federal funding for security in state and local facilities, and bonds in local school districts,” wrote No 17, Preferred Technology LLC, SDM’s 2023 SDM’s 2023 Systems Integrator of the Year. “With crime on the rise in all three of our geographic areas, many customers are looking to increase their security. With the increases in legislation for funding, we anticipate more local governments, public schools, and universities adding or upgrading their systems.”

No. 98, Dehart Alarms Systems LLC, wrote: “We look for 2024 to be a volatile year due to it being an election year and the uncertainty of when and by how much will the Fed lower interest rates. However we do expect there to be an increase in the commercial market driven by the desire for better security, which will be fueled by AI.”

Again and again, respondents noted the impact, particularly of AI, but also other newer technologies as well as the challenges they present, which will likely be a common theme going forward as the rate of technology changes continues to accelerate.

“The security industry faces significant changes, driven by technological advancements and economic recovery,” wrote No. 11, Unlimited Technology Inc. “Success will depend on the industry's ability to adapt quickly and understand market and technology trends.”

.png?height=200&t=1656505078&width=200 "2022-tsi-report")